Does corporate tax avoidance in Europe cost €160-190?

23Jun16

Interviewees for jobs at Google are famously are asked fiendish questions like “how much does the Empire State Building weigh?” or “how many piano tuners are there in Chicago?”.[1] The point of these ‘Fermi questions’ is not that there is a right answer, but that quick thinking applicants can combine the knowable (the population of Chicago), with the guessable (how prevalent is piano ownership? how often are they tuned?) and come up with plausible order-of-magnitude estimate.

The state of the art in estimating the cost of tax avoidance is somewhat similar. There are few known quantities, and the terms and concepts in the question are often vaguely specified. The impact of these numbers though, is more significant than a job interview brainteaser, as they shape the debate around how to strengthen and modernise international tax systems. All too often, even when carefully caveated, the numbers get picked up and used in ways that inflate their scale, and which allow rough guesstimates to be mistaken for empirical findings.

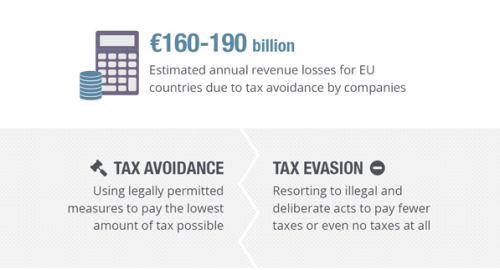

“€160-190 billion”…really?

In the run up to the final negotiation of the EU Anti-Tax Avoidance Directive last week the European Parliament put out a statement and infographic that “Tax avoidance by companies cost EU countries €160-190 billion in lost revenue a year”.

The number is drawn from a research paper which was commissioned by the EU Parliamentary Research Services and written by Dr Robert Dover, Dr Benjamin Ferrett, Daniel Gravino, Professor Erik Jones and Silvia Merler. If you are interested in the issues the paper is worth reading in full. It also includes the data used in the calculations.

One thing you will notice (it is the first line of the abstract) is that the authors do not say that tax avoidance costs €160-190 billion at all. Their core estimate is €50-70 billion. They offer the €160-190 figure as an ‘overestimate’ based on a second, simpler methodology.

The explanation for these numbers on pages 13-16, although it is a little hard to understand. This blog post (which draws on discussions with the tax blogger Fairskat (Rasmus Corlin Christensen) and Iain Campbell of ARC, as well as with two of the authors Bob Dover and Erik Jones) is an attempt to clarify the basis for the two sets of estimates before the €160-190 figure passes into folklore.

Estimating tax gaps

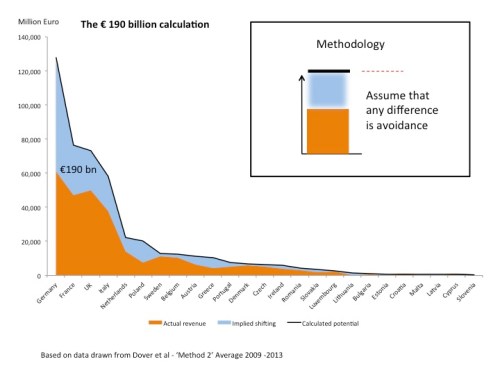

The basic idea for estimating the cost of tax avoidance is to compare the amount of tax revenue that is collected (the orange area) with the amount that would be collected if the avoidance behaviours did not happen (the red line).

However in practice such top-down estimates are notoriously unreliable and prone to pitfalls. The word ‘avoidance’ can mean many things to many people, so first there is the problem of establishing a clear definition. Then there is the problem of estimating the counter-factual tax bill from sparse and imperfect data.

Dover et al. describe aggressive tax planning and tax avoidance as ‘ostensibly legal practices [..] using often sophisticated business and accountancy practices to minimise a company’s tax liability’. They estimate their scale by drawing on data from national accounts as a gauge of the total net value-added generated by for-profit companies in each country. They take this as a proxy for taxable corporate profits and multiply it by the headline corporate tax rate in each country to calculate the corporate income tax potential.

They note that the gap between this number and what is actually collected will include factors such as accounting differences between the ‘assumed’ and ‘true’ tax base, legislated tax incentives and reliefs, and weaknesses in compliance and enforcement, as well as avoidance.

Putting a number on it

The € 160-190 billion figure is reached by ignoring these real-world factors and simply taking the whole of the gap between the calculated potential and the tax revenue collected as avoidance through international profit shifting.

€190 is clearly an overestimate, as the blue area includes things that are not just ostensibly legal, but uncontroversially legal: things like differences between capital allowances for tax purposes and way that ‘consumption of fixed capital’ is reported in national accounts, double tax relief under tax treaties, tax exemptions for Real Estate Investment Trusts and corporate charitable donations and tax incentives for things like R&D, energy efficiency and employment (in the UK, Netherlands and France respectively).

The core estimate of €50 – 70 billion is based on a methodology that seeks to take account of these ‘other factors’ – i.e the grey, pink and green shaded areas, by allocating 25% of the estimated tax potential in each country to cover them.

It is a very simple, very rough way of trying to put a number on avoidance. But it is essentially a guesstimate – since it is not based on any additional data on actual tax reliefs, tax incentives or tax collection inefficiencies, but simply assumes a common rate between countries. The research team chose the 25% based on the observation that the average ‘tax efficiency’ in their sample (i.e. actual revenue as a percentage of potential at a country level) is 75%. However this is based on efficiency levels which range from 7% to over 200% (in the tail of the chart above) — which is hard to reconcile with either real world (how does a country collect over 200% of the tax due?) or with the assumption of that the average then reveals a meaningful indicator of underlying efficiency common to the whole sample.

It may be that the core estimate of €50 – 70 billion is too high – for example Rasmus calculated that if ‘other factors’ amounted to for 50% instead of 25%, then the estimate of tax avoidance would fall to €25-35bn [2](and indeed the authors say that a complete solution to the problem of base erosion and profit shifting would have positive impact of 0.2 per cent of the total tax revenues of the Member States – or around €12 billion – which is a rounding error on the overall tax take in Europe of €5.7 trillion). On the other hand the figure could be too low: many specific international tax controversies are excluded by the data. For example that Google sales to customers in the UK are booked in Ireland, or that McDonalds in France pays royalties for use of the franchise to McDonalds in Luxembourg is not captured in the paper’s calculation at all.

What is clear (as the authors point out) is that the previous go-to number in shaping expectations €1 trillion, is wildly out of whack. It has often been used to represent as the scale of corporate ‘tax dodging’ in Europe including by Herman Van Rumpuy, the European Commission, MEPs, José Manuel Barroso, the media and NGOs, but is based on a misreading of another estimate which is mainly about something else altogether.

Given this context of previous inflated expectations, and the levels of uncertainty in the estimation, does it matter that the European Parliament chose the larger number to promote, even though the paper points (albeit cautiously) to the smaller one?

I would say yes. This is an area where there is so much noise, misunderstanding and partisan information, that when an organisation like a Parliamentary Research Service steps in, the simple expectation is that they should do their best to provide independent, objective and authoritative public information, (even in infographics). A larger number and apparently greater certainty may be better for political momentum, but more realistic understanding is better for guiding the effectiveness of the response.

[1] At least they used to, apparently not anymore

[2] Rasmus’s spreadsheet, based on the annex tables in the paper

Filed under: Uncategorized | 1 Comment

A review of tax gap methodologies and a calculation of Oz LM Inc Tax gap in https://www.academia.edu/13853681/Regulatory_Compliance_Case_selection_and_Coverage_-_Calculating_Compliance_Gaps