2.7% of GDP: another big number to take with a huge pinch of salt on multinational tax avoidance in Africa

24Apr19

The United Nations Economic Commission for Africa report on Fiscal Policy for Financing Sustainable Development is a serious piece of work. But it contains the latest in a long series of silly numbers which inflate perceptions of the scale of revenue at stake from multinational corporate tax avoidance.

It says tackling base erosion and profit shifting by major multinationals in Africa could boost tax revenue by an estimated additional 2.7 per cent of GDP. That works out at around $60 billion, bigger still than Kofi Annan’s much repeated big number from 2013 (which was based on a misunderstanding of a whole different set of numbers) and more than current levels of annual inward FDI.

Where does this number come from? Is there any reason to think its the right number now? And if not why does nobody notice?

The paper references the number as coming from Alex Cobham and Petr Janský’s 2018 paper Global distribution of revenue loss from tax avoidance in which they recalculated the Ernesto Crivelli, Ruud De Mooij and Michael Keen’s finding from the 2015 IMF “Spillovers” working paper . The IMF working paper came up with a figure of 1 percent of GDP. How do UNECA they get to 2.7 percent? I don’t know. Cobham and Jansky say that the average revenue loss they calculate across the African countries in their study is 2 percent of GDP (and this is what I get from adding up their figures too). I have no idea how UNECA made it up to 2.7 percent.

And as Cobham and Jansky notes the Crivelli, De Mooij and Keen methodology is quite mechanical: for the country level estimates you plug in the statutory tax rate and it spits out an estimate of the revenue loss. On this basis Chad is said to be losing tax revenues worth some 8 percent. The way the methodology works the only thing you can conclude from Africa having a higher headline figure than other developing regions is that statutory tax rates are higher. As I have highlighted before these estimates are much bigger (by an order of magnitude) than anything revealed through micro-studies or audits, and from Gabriel Zucman’s estimates.

The UNECA report specifically names the extractive sector as the culprits for the 2.7 percent (although the Crivelli, de Mooij and Keen methodology excludes natural resource rich countries in developing its model, because it says their revenue drivers are likely to be different)

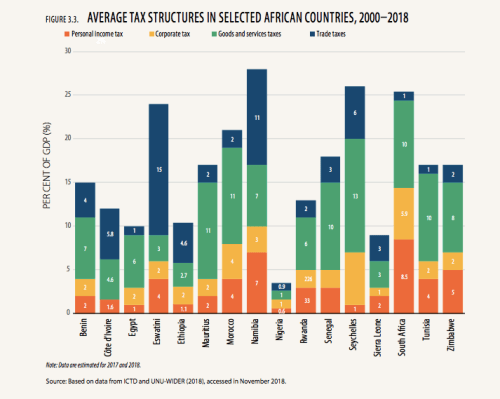

The UNECA Report itself gives some context that ought to have led the authors to wonder about the claims it was making, and whether they were in the right ballpark. It says African countries collect an average of 17 percent of GDP as tax, but could collect around 20 percent. Revenue from corporate income tax is tends to be around 2% of GDP.

So in this context EUNECA’s figure is making the claim that that 90% of the additional revenue potential could come from taxing multinationals, in a move that would more than double their current tax bill (and don’t worry about whether this will impact on investment levels).

In fact the rest of the report does not say that at all. It talks about tax administration efficiency and cooperative compliance, and property tax and personal income tax and VAT. They say that African governments must widen the tax base by bringing hard to tax sectors into the tax net and reassess tax incentives.

But still no one blinked at the big number for BEPS.

The report says that the scale is confirmed by “other estimates of losses through base erosion and profit shifting ranged from 1 to 6 per cent of GDP” referencing this to Taxing Africa by Taxing Africa: Coercion, Reform and Development by Mick Moore, Wilson Prichard and Odd Helge Fjeldstad. I cannot find the 1 to 6 percent figure in the Taxing Africa book. They do reference the IMF working paper’s 1% figure (but I wish they had examined it), anyway its not another independent datapoint. Moore, Prichard and Fjeldstad make the point:

“While international tax rules are deeply important for African states, and their inequity deeply troubling, it remains the case that the greatest potential for improving outcomes still lies in strengthening domestic tax systems on the continent. International tax rules and multinational corporations present easy and attractive targets for criticism by advocacy organisations. In recent years, these criticisms have been very effective in broadening awareness of the issues and encouraging some reform. But there remains a risk that a focus on international tax issues may distract attention from major domestic challenges, which African leaders have sometimes been slow to address. For every MNC evading taxes internationally, there is also a domestic firm benefitting from unjustified tax exemptions (Chapter 6). For every wealthy African with assets hidden overseas in Switzerland or Luxembourg, there are several others avoiding taxes at home in relatively plain sight and without repercussions.”

When I started noticing and writing about these big numbers (which feels like a long time ago) I thought that perhaps better peer review of these reports would solve the problem of these runaway expectations. But the UNECA has an impressive list of peer reviewers. It benefited from background papers from among others Clement Migai and Jeffery Owens at Vienna University and Mick Moore at the International Centre for Tax and Development and it gives a long list of reviewers who provided comments as well as an internal quality control panel and two external review sessions including from reviewers from Ministries of Finance, Revenue Authorities, ATAF, the IMF and several universities.

And still no one noticed.

Of course if they had asked me I’d have pointed it out for them. But they didn’t, and anyway relying on one person to repeatedly tell people that these great expectations are out whack with reality is not a sustainable strategy.

Even when there is no good reason to believe them these ‘great expectations’ have too much politically salience in both developing countries and donor countries and with both international organisations and civil society for anyone to properly question them. But if tax policy is going to support economic growth it cannot be based on economic wishful thinking.

Filed under: Uncategorized | Leave a Comment

No Responses Yet to “2.7% of GDP: another big number to take with a huge pinch of salt on multinational tax avoidance in Africa”