38.4 billion is a very big number – but what does it mean?

09Sep13

Tax transparency has risen up the international agenda over the past few years. Last week G20 leaders took steps in backing international action, as campaigners called on them to ensure that African countries benefit from the global trade in oil, gas and minerals. The headline issue linking the two was transfer mispricing.

Making a link between murky tax dealings by big multinationals and the plight of poor nations struggling to provide healthcare and education is a perfect soundbite. David Cameron only needs to say “tax avoiders should wake up and smell the coffee” and we can dog whistle the rest.

But what if the story we are being told is factually wrong? Is it just pedantry to worry that the numbers and examples used are misleading, so long as they point the spotlight on the important issue of natural resource governance and the need for healthy public revenues?

Public debate on international tax reform revolves around big brands and big numbers. These two strands are increasingly woven together into a single narrative which runs like this:

“Everybody knows that Amazon, Starbucks, Google and co. are dodging taxes. It may be legal, but it is wrong. Multinational companies are doing the same and worse in poor countries, with billions lost to the public purse each year. Closing loopholes would enable more money to be collected and spent on health and education.”

Oxfam made the case earlier in the year in infographic form.

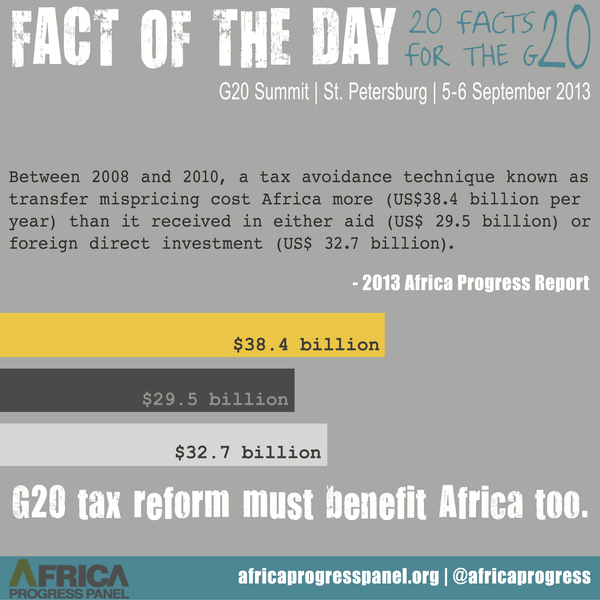

In the run up to the G20 both Oxfam and the Africa Progress Panel again highlighted corporate tax dodging through exploiting transfer pricing which, they both agreed, costs African governments $38.4 billion a year in lost revenues. Kofi Annan reiterated the $38.4 billion number saying that

one single tax avoidance technique – transfer pricing – costs the continent more than it receives in either international aid or foreign direct investment.

But the thing is the $38.4 billion number isn’t about transfer pricing or mispricing at all.

A significant proportion of international trade takes place within subsidiaries of multinational corporations. Transfer pricing is the accounting practice used to allocate costs and revenues between them for tax purposes when they trade internally. Transfer mispricing occurs when companies evade taxes by over or understating the value of goods, services, interest, insurance and royalties, shifting profits into low tax locations.

The Africa Progress Panel Report gives the source for the transfer mispricing figure as the Global Financial Integrity (GFI) report Illicit Financial Flows from Developing Countries: 2001-2010. GFI use IMF Direction of Trade statistics to calculate illicit financial flows. They explicitly state that these estimates do not capture transfer mispricing between branches of multinational corporations. What they seek to assess is false invoicing between unrelated companies for the purpose of money laundering and the payment of kickbacks to corrupt executives or officials. GFI describe the process;

Let’s say I’m a South Africa-based factory owner and you’re a solar panel salesperson from New York City. I want some solar panels to make my factory more self-sufficient, and we agree I’ll pay you $1 million for them. But I ask you a favor: Could you invoice me for $1.2 million and then deposit the extra $200,000 that I just gave you into another company’s bank account in New York City. You’re eager to close a big sale, so we agree to the deal.

You might know false invoicing is illegal, you might not, but it’s very unlikely either of us gets caught anyway. What you don’t know is that I actually made most of that $1,200,000 from my side business, smuggling poached elephant ivory to China; the money I’m about to wire into your bank account comes from my Canary Islands bank account where I send all my business earnings to minimize tax obligations; and I’m going to use that $200,000 to purchase stolen art from a broker in midtown Manhattan so I can decorate my future retirement home in the Seychelles, where another company I control anonymously just purchased some beachfront property

This kind of false invoicing is fraud. It is criminal. It is simply not the same as transfer pricing (or even mispricing, which also carries penalties). Undoubtably, if they are not absolutely scrupulous about compliance, big international corporations can engage in money laundering, and false invoice fraud. But, for example, when Eric Schmidt defends Google’s tax affairs as being ‘just capitalism’ he is talking about how it organises its international operations, not saying it is ok to issue false invoices in order to pay bribes and kickbacks.

I am not a tax expert, but I think the conclusion is unavoidable that the $38.4 billion figure has been misrepresented (perhaps mistakenly?) in referring to tax loss from transfer mispricing. GFI’s estimate does not refer to a tax loss, but to an illicit flow. It does not refer to transfer pricing within companies at all. And it says nothing about the size of the companies involved.

Similar criticisms have been made of the much quoted $160 billion global ‘big number’ about tax avoidance (which is based on a similar approach).

The two problems of false invoicing and transfer mispricing are not unrelated, but they are not the same. It is like talking about malaria, using figures that really relate to HIV.

I think that part of the reason why these estimates have been applied to the ‘wrong disease’ is that the debate on international tax is so partisan. Details of definitions and tax law tend to be shrugged off as clever talk from big corporations and big accountants defending their own interests (which, of course they are, but they do have some expertise, and ‘skin in the game’ of development).

Another reason is that the big numbers confirm what ‘everybody knows’; that big corporations are all engaged in transfer mispricing, (just look at Amazon, Google and Starbucks …)

But the thing is, Amazon, Google, Starbucks et al are really not great as poster children for transfer mispricing either. Experts who have been through the numbers (including presumably the tax inspectors, otherwise they would be in court) say that they are operating within the letter and the spirit of the law charging ‘arms-length’ prices between subsidiaries (for example for a good summary of the Starbucks case see Ben Saunders’ blog).

An argument can be made that the transfer pricing system itself is immoral and unworkable, or that there are specific loopholes that should be closed, but these cases in themselves don’t illustrate companies getting away with transfer mispricing.

None of this means that the case for better regulation, stronger enforcement, international collaboration and transparency should be dismissed. Illicit flows, tax evasion, and the need to bring taxation systems up to date to reflect globalised trade and intangible assets are all real. But if we are serious about these things evidence has to trump narrative.

For example recent research by Christian Aid sought to use international trade data to find out how much tax multinational corporations were avoiding through transfer pricing in India. Instead they found out that multinationals (including those with links to tax havens) were paying higher effective tax rates than domestic companies. That surprising finding is mentioned briefly on page 9 of the report, titled Multi-national Corporations and the Profit Shifting Lure of Tax Havens (I asked if they could share that part of the analysis, but they said they couldn’t).

The Africa Progress Panel is a good initiative and in general an excellent report. It highlights the range of factors facing African countries in ensuring that the growth of extractive industries translates into improvements in the lives of people. Domestic leadership and governance, public spending and economic policies and competencies and institutions are hugely important. A key factor in determining how the value of natural resources is distributed between government and foreign investors is the contracting process. The report includes several examples of governments signing away concessioning rights under ‘staggeringly poor terms’. For example, recent deals in the Democratic Republic of the Congo cost the country an estimated US$1.36 billion through the systematic undervaluation and sale of nationally owned mineral assets. Developing effective approaches to encouraging and requiring local economic linkages is also crucial. Transfer pricing is only one factor (interestingly, it barely got a mention in the expert consultation identifying issues).

As Paul Collier and others have acknowledged , the public anger around the high profile tax scandals has been a boon to the development community in communicating otherwise dry issues like the call for beneficial ownership registers. In this context, does it matter if the numbers don’t quite mean what we are told they do, or the wrong companies are vilified?

I think it does. Broad brush estimates played a role in raising awareness, but continuing to use them in misleading ways undermines public understanding, and distorts the debate.

Rebranding estimates of illicit flows under the headline of corporate tax evasion, makes one problem seem to go away, and does not advance our understanding of the other.

The always attractive conclusion that its-all-the-fault-of-multinationals oversimplifies complex issues, takes the heat away from governments, may lend support to local actions that create uncertainty in investment environments already seen as risky, and stands in the way of working out solutions to address the natural resource curse with the private sector.

The issue of how multinationals and their home governments can best contribute to sustainable development in the countries in which their invest and trade is serious. Understanding the patterns, issues and trade-offs involved requires rigour, both in the research that is done, and the way it is reported.

Filed under: Uncategorized | 7 Comments

Last night I spoke with some of the team at Global Financial Integrity and they confirmed to me that their estimates (which are the source of numbers quoted by Africa Progress Panel and Oxfam) do not relate to transfer pricing within multinational corporations.

What their estimate is designed to capture is mispricing through re-invoicing involving two unrelated companies which they describe here:

This is what the $38.4 billion number relates to. They also confirmed that, although reinvoicing is used as means of tax avoidance and sometimes evasion, the estimate itself should not be interpreted as a tax loss, because only a portion of it would have been due as tax. They have a methodology for roughly estimating the implied tax loss which involves multiplying the financial flow by the tax rate in each country.

They did say I made one mistake in my post, and I want to correct that. The hypothetical case which I quoted about the solar panels is actually an illustration of ‘same invoice fraud’ which also can not be captured by the GFI estimates.

I can’t find a hypothetical example of reinvoicing in the tax transparency literature, but there are lots on the websites of companies that sell this kind of service, so I include one here:

“An exporter corporation sells $1.000.000 of exports to France normally every year. Assuming cost of goods sold and operating expenses are $600,000. the exporter corporation earns $400.000 on its sales before taxes. Taxes will average say $160.000 thus reducing net profits to $240.000. The exporter establishes a tax haven corporation to act as intermediary managed by […] . The exporter corporation sell its products to the tax haven corporation on paper for say $600.000. The tax haven corporation in turn sells the goods to the French client for $1.000.000. The tax haven corporation, thus earns $400.000. Since there are no taxes, $400.000 is the net income after taxes. The exporting corporation shows no profit. ($ 600.000 gross sales less $ 600.000 cost of goods sold).”

GFI’s estimates actually find that Sub-Saharan Africa suffered average annual illicit financial outflows due to trade misinvoicing of US$40.27 billion per year over the three year period of 2008-2010. Although trade misinvoicing and illegal transfer pricing may provide similar incentives, our illicit financial flow estimates are only able to detect fraudulent misinvoicing through a process called re-invoicing. While reinvoicing tends to predominantly happen between unrelated parties, it does sometimes happen between related parties. Whether it happens between related or unrelated parties, it is detected in GFI’s methodology, but we are unable to distinguish between the two.

If, for example, a Ugandan businessman wants to sell $15 million worth of widgets to an American buyer, he can instead invoice the transaction at $10 million to a tax haven entity and have that entity reinvoice to the American at $15 million. When the American pays the $15 million to the tax haven account, that account then pays the Ugandan businessman the $10 million originally invoiced. Hence, the businessman has moved $5 million offshore, untaxed and unutilized for business or development purposes. And from the tax haven account the businessman can move the money wherever he wants for other investment or consumption purposes, unknown to Uganda government officials and most likely unknown to others in his country.

Why is the businessman doing this? He may be trying to avoid taxes, or he may be trying to hide illicit money that has been illegal earned, transferred, or utilized. We are unable to distinguish between the various motivations. We know from anecdotal evidence that trade misinvoicing is used by a range of criminals, from corrupt public officials to terror groups to drug cartels, to move or launder illegal money.

This process can be measured quantitatively by utilizing bilateral trade data reported by governments to the International Monetary Fund’s (IMF) Direction of Trade Statistics database. In the preceding example, the Ugandan customs will report the $10 million transaction to the IMF, however the American customs will report the same transaction as being worth $15 million. The gap between these two figures, after adjusting for the cost of insurance and freight, is the amount of trade that has been re-invoiced.

That said, our trade-misinvoicing methodology does not detect same-invoice faking, which is what many multinational corporations would use to internally engage in abusive transfer pricing, profit shifting, and tax avoidance.

When one arm of a multinational company manipulates the price of a commodity that it sells to another arm of the same multinational company in an effort to shift profits to a low- or no-tax jurisdiction, the same distorted price appears on the customs invoice filed in both the exporting and importing country. As such, when GFI compares the prices reported by importing nations and exporting nations in this scenario, there is no discrepancy, and the mispricing goes undetected.

However, it is not accurate to state that all same-invoice faking is abusive transfer pricing, as criminal organizations and corrupt politicians can also utilize it to launder their wealth around the globe.

GFI’s trade misinvoicing methodology detects fraudulent trade transactions that have been re-invoiced. While this tends to be used more by unrelated parties, it can be used by related parties—such as two branches of a multinational corporation—to shift money around the world. GFI is unable at this time to detect same-invoice faking in its methodology—which tends to include many abusive transfer pricing transactions utilized by multinational corporations to dodge taxes.

GFI is also only able to measure misinvoicing that happens with trade in commodities and goods. Our methodology doesn’t detect mispricing of services, as there is no comparable database to the IMF DOTS for services trade. This means that any mispriced consulting fees, royalties, or intellectual property fees go undetected in GFI’s methodology. Case studies on many multinational corporations, particularly pharmaceutical and technology companies, indicate that they utilize abusive transfer pricing in services to shift much of their profits to low- and no- tax jurisdictions. None of those transactions are detected by GFI’s data.

Given all of the types of illicit trade transactions that are not captured by our trade misinvoicing methodology, we believe that our trade misinvoicing numbers are extremely conservative.

________________

***Brian LeBlanc is a junior economist at Global Financial Integrity in Washington, DC***

Update: Action Aid are now reporting that: “The Africa Progress Panel estimates that lost taxation is costing sub-Saharan Africa US$63 billion every year. This lost tax, if paid and targeted effectively, would be enough to reach the UN’s millennium development goals of universal primary education and universal healthcare, with enough money left over to upgrade Africa’s entire road network, boosting regional trade and local development.”

The figure of $63 billion is a misreading of a graph from the Africa Progress Panel report (http://www.africaprogresspanel.org/wp-content/uploads/2013/08/2013_APR_Equity_in_Extractives_25062013_ENG_HR.pdf – page 66).

Action Aid have added together the Africa Progress Panel’s misunderstood $38.4 billion number with an estimate for ‘other illicit flows’ ($25 billion: also not a tax loss) and represented the total as being money missing from the the public coffers.

I wonder if they will be correct it, or if another zombie number will be allowed to live on to confuse the debate?