Country by Country Reports: Who is Exchanging with Whom?

04Sep17

What does CBCR information exchange have in common with a tartan laundry bag?

Action 13 of Action Plan on Base Erosion and Profit Shifting (BEPS), calls for multinational groups with revenues over 750 million Euros, to produce a ‘country by country report’ (CBCR) detailing their profits earned and taxes paid, in each country of operation. The aims is for revenue authorities to use this information as a risk assessment tool to direct their audit attention. As Pascal St Amans, at the OECD put it

“tax administrations will be able to identify very clearly, in a single document, whether or not they “smell a rat,” such as where, for example, you have all your profits in a zero tax jurisdiction where you have no sales, no employees and no assets”

To date 102 countries and jurisdictions have joined the BEPS Inclusive Framework, and are at various stages of establishing domestic legal frameworks, as well as bilateral agreements to automatically exchange the reports with other revenue authorities. Ultimately this means that some 10,000 bilateral relationships will need to be established. But not all of these linkages are equally important – the critical information flows will be between countries where multinational groups are headquartered and those where their subsidiaries are.

So who is exchanging with whom?

64 countries have signed up to the OECD’s Multilateral Competent Authority Agreement on the Exchange of CbC Reports (the “CbC MCAA”), which provides a standardised mechanism for making these agreements. However this does not automatically lead to information exchange; each pair of countries has to nominate each other in order to ‘activate’ their relationship. Some countries such as the United States are not using the multilateral instrument at all, but are establishing their own bilateral agreements one-by-one. Some countries such as Vietnam are by-passing the exchange of information system altogether and requiring that multinational subsidiaries file a copy of the CBCR report from their parent company directly with the local tax authority.

Multinational corporations are concerned about the development of this complex network of arrangements, because if agreements are not place in time before the first exchanges are due to take place this year, then companies may be required to supply reports directly to local tax authorities. As Bloomberg BNA reports this raises concerns about confidentiality;

“If the information leaks, the consequences for multinational companies are dire: trade secrets made available to competitors, criticism in the press and harm to customer-facing businesses.”

NGOs on the other hand are concerned that developing countries will be left out of the loop of exchange of information and that countries will ‘cherry pick’ those that they will exchange with.

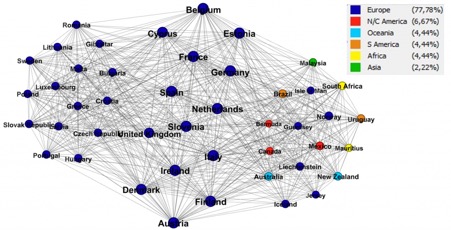

The OECD provides online access to its database on the evolving network of activated relationships, and there have been a few efforts at visualising it. Rasmus Christensen got there first with a nifty network diagram.

Source: Rasmus Christensen, by kind permission

Wouter Lips put the network onto a world map, where it turned into a flower.

Source: Wouter Lips, by kind permission

What both of these data visualisations show is that agreements to exchange information are densely concentrated in Europe. This is not surprising since EU member states have all agreed to exchange together through an EU Council Directive (2016/881/EU).

What else is going on?

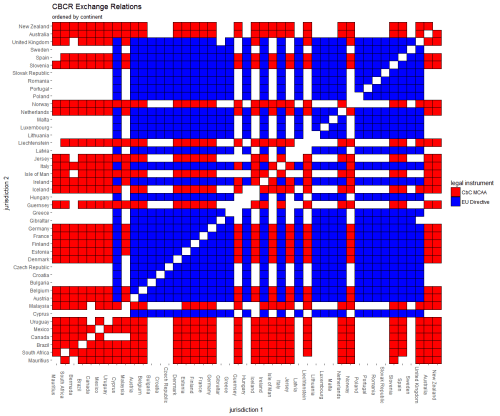

I asked Wouter if he could come up with a heatmap diagram of the state of bilateral relationships and he produced this fetching tartan design.

Source: Wouter Lips, by kind permission (Interactive version)

The tartan pattern is telling – it suggests that countries are not cherry picking partners individually but tend to be following a few general rules, which make up the warp and weft of the pattern. EU countries are all connected (the blue square). Countries that are seeking to activate MCAA relationships seem to be activating exchange relations in general with others that are also active (making red stripes). There are a few exceptions where countries have not activated relationships, which stand out like dropped stitches against the pattern. There are some EU countries (such as Sweden, Luxembourg and Croatia) that have not yet actively sought to exchange with any other countries outside of the EU (this creates the white stripes).

However Wouter’s tartan does not include the countries that are not yet exchanging at all, so it does not give the full picture. Nor does it include the US which is negotiating agreements to exchange.

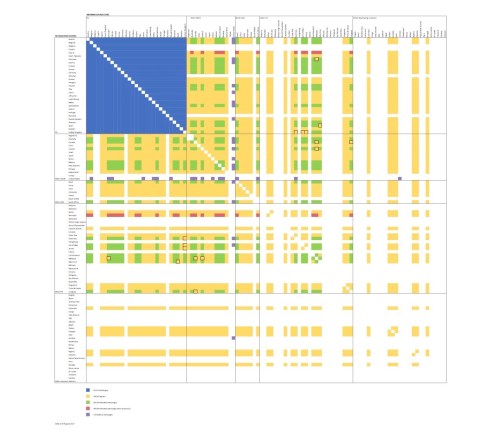

Here is my iteration. It looks less like tartan and more like a map of Manhattan (explore the larger version )

Jurisdictions acting as recipients of information are along the top. Jurisdictions in their role as senders of information are along the side. The countries are arranged in groups according the clubs they are member of; from the top left; EU members, other OECD members, other G20 members, and non G-20 members (split into countries included in the ‘financial secrecy index and other developing countries.I have also included the US’s bilateral agreements, which for are not included on the OECD database.

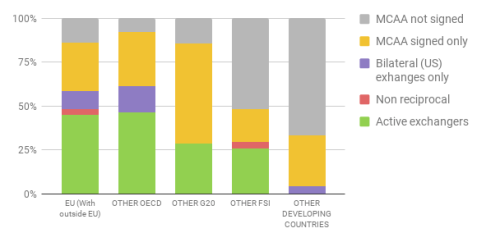

The yellow bands are countries that have signed up to the MCAA but have not yet secured active agreements. The distribution of the green, yellow and white bands across the neighbourhoods reflects that OECD and EU members are most active at signing up to the MCAA and activating exchange relationships followed by others in the G20. Jurisdictions which feature in the financial secrecy index have activated more exchange relationships than other non G20 countries (perhaps reflecting that these countries tend to be more engaged in international investment flows, and also that they have reputational reasons for being early adopters).

Approach to establishing CBCR exchange relationships to date (% by group)

The top sharing nations to date are Belgium, Estonia, Ireland, Netherlands, Australia, New Zealand, Norway, Brazil and South Africa. Austria, Finland, France, Germany, Italy and Slovenia have also activated MCAA arrangements with all other countries that appear to be actively nominating within the multilateral framework. The UK similarly has activated agreements with all other active MCAA participants on the chart (apart from CDOTS). The US is rapidly building up bilateral exchange relationships with 20 already signed and 20 in negotiation.

Number of exchange relationships (August 2017)

There are a few exceptions to the overall pattern of countries within the MCAA system matching up with all other active participants:

- Bermuda is a ‘non-reciprocal country’; that is it will share CBCR reports with other countries but does not require them to share with it (this makes sense as Bermuda does not levy corporate income tax)

- Cyprus appears to be responding to all requests to activate relationships, but is also not requiring other countries to share with it (i.e. it is non reciprocal beyond the EU block).

- There are a few other non-sharing pairs (outlined in black), Canada, Denmark and Iceland and are not sharing with Malaysia; Bermuda, Spain and Lichtenstein are not sharing with Mauritius; Cyprus, Malaysia and Uruguay are not sharing with Canada

- The UK seems to have agreed not to exchange with its ‘Crown Dependencies and Overseas Territories’ – Bermuda, Jersey, Guernsey, The Isle of Man and Gibraltar (presumably since these jurisdictions do not levy corporation tax and are not expected to be the home jurisdictions of the parent entities of multinational groups).

The US has agreed bilateral information sharing arrangements with several big sharers such as Belgium, the UK, Australia and Norway, but also with a few countries that are not yet exchanging with anyone else such as South Korea and Jamaica, and is in negotiations with several more countries including India and Colombia.

Of the top ten sources of foreign direct investment globally, five have activated some exchange relationships (US, Netherlands, UK, Germany and France), Luxembourg has only activated relationships as required by the EU Directive, but is in negotiation with the US, and four countries (Hong Kong, Japan, British Virgin Islands and Switzerland) have yet to activate any relationships.

Several middle-income developing countries have activated exchange relationships (Mexico, Brazil, South Africa, Malaysia, Mauritius), but while many developing countries have signed the multilateral agreement, no developing countries outside of the G20 and the FSI list have so far succeeded in activating relationships through it. This may be because they are not ready and this is not a priority, so they have not sought to nominate any partners yet, or it may be because they have nominated but none of the other countries have accepted.

Both NGOs and the business community are worried about the messy transition from this first set of agreements to full implementation of CBCR – companies are worried by the risk of leaks and misuse of information, while NGOs are concerned that ‘no country gets left behind’. Countries are keen to be part of the Inclusive Framework, but may have other priorities than development of the system needed to assure confidentiality of these reports – particularly where it is not yet clear how these investments will pay-off. The recently published African Tax Administrator’s Forum (ATAF) 2017 Africa Tax Outlook report, for example does not mention exchanging CBCR reports as a priority.

The race to develop bilateral relationships to avoid local filing requirements is built into the design of the mechanism, and is helping to bootstrap the rapid growth of the network of CBCR network. However the process of learning how CBCR reports can effectively be used by revenue authorities is likely to be a slower cycle of iteration (particularly for countries that are starting further back in terms of the development of audit capacity and transfer pricing rules). It does not depend on every country having a comprehensive set of bilateral exchange agreements in place on the starting date, but in 80:20 fashion on the agreements with the countries that are the most important sources of FDI investment, and on the ability to use the information to inform effective audits. These developments are likely to proceed through iteration. Capturing and sharing learning from the early adopters of CBCR reporting over the first few cycles may be more important than getting everyone linked together at the outset.

Filed under: Uncategorized | 1 Comment

Maya, an excellent update on a hard-to-track and complex topic, thank you. Lots of work ahead for many countries.