Reckitt Benckiser: Profits vanishing?

09Aug17

Reprinted with permission from Tax Journal. (PDF version)

Reckitt Benckiser (RB), maker of household products from condoms to stain removers, is the latest company to come under fire for tax avoidance. Oxfam published a report on 13 July, saying the company has been ‘making tax vanish’ by shifting profits to its regional hubs in the Netherlands and Dubai. The company refutes this, saying that its group structure is designed to serve its worldwide markets most effectively. RB highlights that in 2016 the group’s overall effective tax rate was 23%, putting it in the middle of the pack amongst its peers. Furthermore, it has published tax principles which commit the company to ‘paying tax where value is created’.

Reckitt Benckiser (RB), maker of household products from condoms to stain removers, is the latest company to come under fire for tax avoidance. Oxfam published a report on 13 July, saying the company has been ‘making tax vanish’ by shifting profits to its regional hubs in the Netherlands and Dubai. The company refutes this, saying that its group structure is designed to serve its worldwide markets most effectively. RB highlights that in 2016 the group’s overall effective tax rate was 23%, putting it in the middle of the pack amongst its peers. Furthermore, it has published tax principles which commit the company to ‘paying tax where value is created’.

If we are to move beyond this familiar cycle of criticism and rebuttal towards clearer debate, we need to take both sides of the argument seriously.

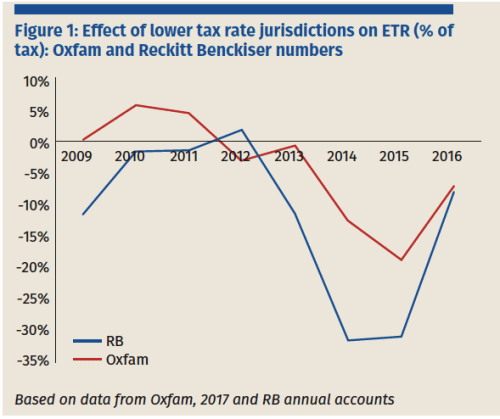

The Oxfam report is thorough, looking at data from RB’s annual reports, as well as accounts filed by some of its subsidiaries, between 2009 and 2016. Over this period, the company reorganised its global operations into three, and then two, regional businesses. Oxfam argues that saving tax was a significant driver for the reorganisation and estimates that RB reduced its tax bills by £200m between 2014 and 2016. Following the reorganisation, it finds that profits fell drastically in several countries. RB France had an operating profit margin of 17% before the reorganisation, which fell to around 6%; Belgium’s operating margin fell from 20% to around 2%; and Australia’s fell from around 28% to less than 10%. Meanwhile, the Netherlands hub accounted for 31% of the group’s profits, with an operating margin of over 45% in 2013 and 2014.

If activities move from one country to another, then transfer pricing rules require this to be reflected in taxable income. However, Oxfam questions whether real activities were moved. RB says that its tax policy is ‘totally legal and the norm for the majority of global businesses’. It argues that the reorganisation was driven by a commercial decision to manage European and North American businesses as one region, and all developing countries as another.

RB does not dispute Oxfam’s finding that operating in jurisdictions where it pays a lower tax rate has had a significant impact on its overall effective tax rate, nor is this hidden. In fact, the company’s own figures indicate that the effect of operating in jurisdictions with tax rates lower than the UK’s was $367m between 2012 and 2016; this is higher than Oxfam’s £200m headline. Both Oxfam’s calculations and RB’s own figures show a similar trend, with lower tax rates reducing RB’s effective tax rate (ETR) significantly in the years following the 2012 reorganisation.

It is hard to reconcile RB’s stated commitment to pay tax ‘in accordance with where value is created’ with these large fluctuations in the effects of lower tax rates. They seem to imply that there must have been significant shifts in the location of where value was created in each year from 2012 to 2016 (or in the tax rates of those places).

So what is going on? Is RB an aggressive tax avoider or a model corporate citizen? Does the case really show that country-by-country reporting is a miracle product that could act as a stain remover on corporate reputations, or does it point to the need for more old-fashioned elbow grease of businesses, tax professionals and their critics coming together to build shared understanding?

Paying the UK rate

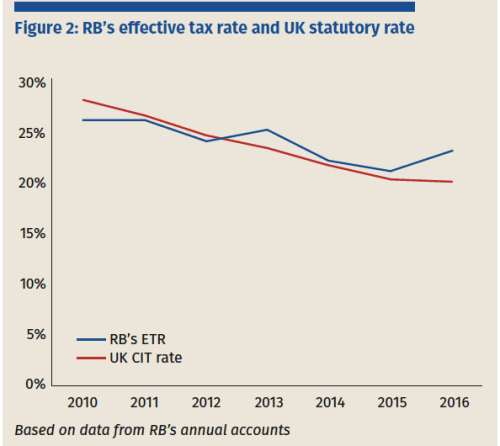

As RB highlights, its effective tax rate of 23% is above the UK headline rate. In fact, RB’s ETR has tracked the UK’s rate quite closely, declining from around 26% in 2010 (although the company pays only around one eighth of its tax bill in the UK).

Perhaps this is a coincidence, or perhaps the company has been managing its ETR with the objective of staying close to the UK rate – seeing this as the implicit benchmark for demonstrating responsibility and avoiding stains on its reputation.

Tracking the UK rate might be viewed as a simple benchmark for responsible tax practice; a company that is paying the statutory rate cannot be a massively successful tax avoider. The Fair Tax Mark criteria for UK based multinationals, for example, takes this approach, giving maximum marks (on this criteria) for companies whose ETR is within 1% of the UK statutory rate. However, as the RB case highlights, this may not be an adequate test.

Benchmarking against a more meaningful rate

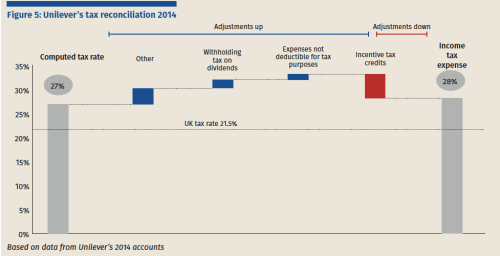

An important area of tax transparency is publishing a tax reconciliation highlighting the factors which explain the difference between a company’s ETR and the relevant statutory rate for its business, such as incentives, carried forward losses, capital allowances and lower tax rates.

RB’s approach of reconciling its tax charge using the statutory tax rate in the territory of the parent company is common. However, achieving an ETR in line with the prevailing rate in the country of its headquarters is not a good guide to whether a global company is ‘paying tax where value is created’. And, as the UK tax rate is lower than the global average, this benchmark will tend to drive profit shifting in other places.

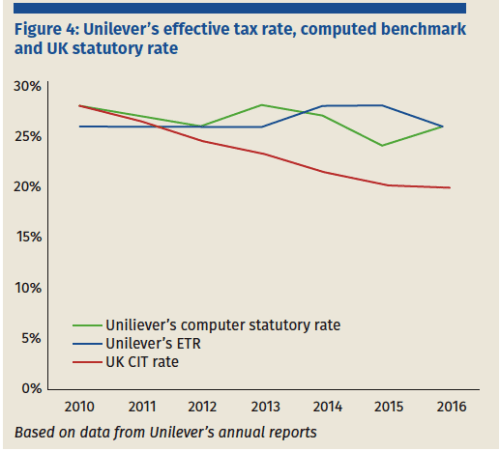

A better approach might be to use a benchmark which reflects tax rates across the territories where the company does business. This is the approach taken by fellow Anglo- Dutch purveyor of consumer goods, Unilever. Unilever reconciles its ETR against a computed benchmark based on average rates of the countries in which it operates,weighted by accounting profits before tax. Even as the UK headline rate fell, Unilever’s benchmark rate has remained between 28% and 24%, and its ETR has remained between 26% and 28%.

Prudential goes further and splits its tax reconciliation into US, UK and Asia regions, setting out clearly how much of the rate is due to statutory rate differences and how much is due to specific tax adjustments in each region.

Truth and reconciliation

The RB case highlights challenges, both to businesses and to tax campaigners. Oxfam’s analysis suggests that there may be a gap between RB’s company principles and its practice (or at the very least it should explain why lower tax rates were so prominent after 2012). Commitments to principles will quickly become devalued, unless they can be backed up by specific criteria and meaningful indicators which show how they are being met.

However, Oxfam’s analysis also suffers from its own gap between perception and reality. As the report outlines, RB was identified after Oxfam reviewed the tax affairs of FTSE 100 companies. If this is the ‘best’ (or worst) case it found, this does not provide support for the popular view that large multinationals are able to run rings around the international tax system and achieve tiny tax rates. Studies looking from the other end of the telescope also indicate that the impact upon developing countries of profit shifting multinationals may be smaller than is often supposed. For example, a recent study in South Africa estimated that multinational subsidiaries shift out 7% of their profits. However, preventing this would only increase the overall tax to GDP ratio by 0.05%.

However, Oxfam’s analysis also suffers from its own gap between perception and reality. As the report outlines, RB was identified after Oxfam reviewed the tax affairs of FTSE 100 companies. If this is the ‘best’ (or worst) case it found, this does not provide support for the popular view that large multinationals are able to run rings around the international tax system and achieve tiny tax rates. Studies looking from the other end of the telescope also indicate that the impact upon developing countries of profit shifting multinationals may be smaller than is often supposed. For example, a recent study in South Africa estimated that multinational subsidiaries shift out 7% of their profits. However, preventing this would only increase the overall tax to GDP ratio by 0.05%.

Given these relatively marginal impacts, perceptions often become inflated. This Oxfam report includes a few familiar moves. It estimates that RB could have avoided around £60m in developing markets over three years, saying that this amount could pay for toilets for more than half a million people in Bangladesh or sewage treatment for the same number Pakistan. However RB’s ‘developing markets’ revenues include large economies such as Argentina, Brazil, China, India, Indonesia, Japan, Korea, Taiwan and United Arab Emirates, so any amount of tax applicable to smaller, poorer economies is likely to be a tiny fraction of the total, equivalent to many fewer toilets. Similarly, Oxfam says that the amount of revenue lost over three years in Australia could have provided ‘funding for over 11,000 secondary school students’. This calculation is only true if each student only went to school for one out of the three years.

The tax debates between multinational companies and NGOs could continue going in circles, with companies making ‘motherhood and apple pie’ commitments, and NGOs believing their own rhetoric of an El Dorado of taxes for the poorest countries. But this risks achieving little, while undermining trust on all sides.

Discussions around specific cases provide an opportunity to move forward, testing claims, assumptions and concepts. The RB case also highlights an immediate practical step which companies could take, without revealing commercially sensitive information. Companies should improve how they explain any difference between their ETR and the statutory rates in the places where they do business. And NGOs, peers, investors and researchers should pay attention to this information, as Oxfam has.

Filed under: Uncategorized | 1 Comment

This is the type of rhetoric free analysis which is the required precursor to have a meaningful debate about a) corporate responsibilities (or lack thereof) regarding tax planning and b) effective domestic and multi-jurisdictional responses. Bravo