Did the UK really agree to charge Google a 3% tax rate?

25Jan16

The settlement between HMRC and Google that the company will pay £130 million in additional back taxes and higher rates of tax in the future is big news here in the UK, and is an early sign of how implementation of the G20/OECD ‘BEPs’ international tax reforms might play out. A common reaction to the announcement that, after a six year investigation Google’s annual UK tax bill has been increased to around £30 million is that it doesn’t seem like a lot ( ‘very small‘….’pitiful‘…minute‘..’derisory‘…’trivial‘….. you get the picture).

It is certainly not a lot compared to popular expectations that tackling tax corporate dodging will generate billions of additional public revenues. And it doesn’t look like a lot compared to Google’s UK revenues (Google reports that about 10% of its revenues – $6.5bn or around £4.6 billion – came from the UK in 2014).

But corporate taxation, of course, is calculated on profits not on revenues. One suggestion that is making people angry at its apparent unfairness, and which supports the view that the settlement is way below what it should be, is the estimate that £30 million represents a 3% tax rate on Google’s UK profits. Professors Prem Sikka and Richard Murphy, and tax QC, Jolyon Maugham have all come up with a similar estimate, and it has been cited today by John McDonnell on the Today show and on Newsnight and by MPs in Parliament.

Jolyon gives a clear outline of the workings on his blog (and many of his much-more-tax-expert-than-me commenters take issue with it). Basically its based on a calculation in round numbers that Google’s reported global profit margin is 25%, so with around £4bn in UK sales must therefore be making £1billion in UK profits and should be pay £200 million a year in tax to HMRC.

But that is not how the tax system works. If a vertically integrated corporation sells cars or bananas, the profit has to be apportioned to different parts of the value chain so it can be taxed in different countries – partly in the country where the cars are manufactured or the bananas are grown, partly in the country where they are sold and partly in the countries where design, marketing, shipping, insurance and financing takes place. The country where the bananas get eaten doesn’t get to claim all the profits for its own tax base.

Google’s business model is that it does a zillion things to be indispensable in our lives, and sells advertising (using Ad-words and youtube adverts etc…) on the back of that, as well as premium services like Google Apps for business. The country where the ads get sold doesn’t get to claim all the profits for its own tax base.

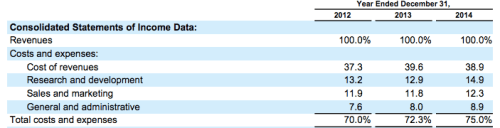

The vast majority of the cool stuff at Google goes on in Mountain View, California. Google’s Annual Accounts don’t give much detail but they do break down global costs into categories:

- Costs of Revenues (38.9% of revenues =52% of costs) is the money they spend on ‘acquiring content’ which means sharing ad-revenues with bedroom superstars like PewDiePie and Smosh, paying royalties for the movies, music and games downloaded through Google Play, driving down every street in the world in a car with camera on top, as well as and running server farms etc..

- R&D (15% of revenues =20% of costs) is building the tech and writing the code to organise all this information

- Sales and marketing (12% of revenues =16% of costs) is selling ads and other services) and (weirdly) advertising Google on the television.

- General admin is legal, finance etc…HR (9% of revenues =12% of costs)

- Which leaves an overall margin of 25% of revenues

Broadly the calculation that Google earns £1 billion profit related to UK sales seems about right, as far as back-of-an-envelope calculations can take us – based on revenues of £4 billion and the overall margin. But the key question is how to divide this profit up between the bits of the business that manage content, write code, sell adverts and keep the whole organisation together.

To come up with the answer that the whole £1 billion ought to be taxable in the UK you have to decide that all of that stuff that goes on at in engineering and design, and in getting millions of people to watch inane or educational stuff on youtube adds no value at, and that 100% of the profits are earned by the hard working sales teams in London.

Or you could decide on principle, that nevermind where the value is created it ought to be taxed only at the customer end of the value chain. But that isn’t the tax system we have now (nor is it obvious its a good idea). So suggestions that Google should have been paying £200 million of UK tax a year appears to be pure wishful thinking.

So is £30 million about right, or is it pitiful and derisory ?

For a more credible-back-of-an-envelope calculation we could attribute the profits to the four activities. For example we could use the same proportions as costs, as a starting point -i.e. 52% comes from its content aquisition etc…, 20% from R&D, 16% from sales and marketing and 12% from admin (of course there are other ways to play around with these numbers, maybe R&D gets more profits, to reflect the risk and long-term payoffs from innovation etc… ).

On this basis we could say that if the UK ought be able to tax the value created by the sales and marketing activities related to UK revenues, then this relates to £160 million of profits (£4bn x 25% x 16%). Tax this at 20% and you get £32 million of revenue – in the ballpark of what was agreed.

(All of this is separate from the question of the Double-Irish-Dutch-Sandwich which is largely about how much tax is paid (or deferred) by Google in the US, and doesn’t affect the amount of tax paid in the UK).

The point of all this is not that we shouldn’t be talking about Google’s taxes, or holding the government to account on how it collects them or thinking about how to change the global tax system for the internet age (we should). But anchoring these discussions with wildly overoptimistic revenue estimates contributes to dysfunctional public and policy debates, and gives the impression that ‘everyone is at it’.

At some point in this debate we are all going to have to ween ourselves off expectations of endless untaxed billions and ground it in economic fundamentals. Now seems as good a time as any.

Filed under: Uncategorized | 16 Comments

The problem in most press coverage is that the people being quoted in the articles are not distinguishing between what is currently legally taxable and what they WISH was taxable. We are then left with the impression that the taxpayer is doing something wrong because they are not paying “the right amount of tax”.

If there was to be an honest debate on the topic, then the players would look to people like you to provide some realistic numbers to consider and then ponder the different foreseeable outcomes of proposals that can realistically be implemented. They may use occasions like this as rallying points “This is the outcome of our current laws so we should change them to have this other outcome”. Instead they prefer to demonise the law abiding and ignore realities like tax competition and the Prisoner’s Dilemma.

Note that Meg Hillier did not call her fellow parliamentarians to appear in front of the Commons Pubic Accounts Committee to explain why they are not considering changing the UK’s tax laws. Rather she DEMANDED that Google appear in front of her committee so that she could try and publicly humiliate them for paying exactly the right amount of tax that Parliament requires. It kind of reminds me of that “She’s a Witch” scene from Monty Python.

I think this is very useful and makes some of those who market themselves as tax experts look a bit silly.

however … I think an estimate should not just be based on getting at the value created by the sales and marketing activities related to UK revenues, but also the content acquisition related to UK revenues – some of those costs are incurred acquiring content for UK consumption.

afaik Google does have some UK R&D but perhaps not significant yet?

Hi Paddy

Thinking about how to tax companies like Google I do think is a significant challenge – all our mental analogies about widgets I think come a bit unstuck when you think about – say someone in the Germany watching a video made by a Spanish vlogger being served an advert for a UK based multinational on a platform whose code was mainly developed in the US but a few other places too, and with the data hosted in on servers in Ireland

(then multiply this by the many possible countries that could be at each node…)

– none of this is complexity for the sake of tax dodging, it is just the underlying business model.

So it is going to be hard to figure out how best to tax it anyway, whether there is tax avoidance or not. I don’t know what the answer is – I guess simpler is better.

understood and agreed. So profit always a construct reliant on a bunch of assumptions, not a natural quantity that can be observed. Question is what do we think realistic UK profit is, in some sense that is meaningful under current conceptions of how to tax MNCs without wishing something like apportionment by sales into existence. I guess many would say letting google get away with selling into the UK from Ireland is not reasonable. On further thought maybe a good basis for a guestimate would strip out costs of content acquisition, because that’s more like a pass through and less like a value creating function, and look at gross profit and then divide gross profit up across countries according to three functions, sales and marketing, technology and IP, and physical infrastructure (data centres). If you did that, big chunk of global profit accrues to US where most tech comes from and IP originated, so you are right the pro-rata split behind the billion is not a sensible benchmark, however I think split on basis of three functions, not allowing UK to be service provider to Eire as it currently is deemed, I guess would leave UK profits a fair bit higher than how you did it. But of course I cannot really claim my back of fag packet superior to yours.

Thanks Paddy, I think your back-of-fag-packet estimate is an improvement on mine.

I think the PE thing is a red herring though. There are [X] number sales & marketing people in Google UK doing their thing. That creates a certain amount of value for the company and earn a certain margin – so the question is is that amount fair enough? Whether they do that through a legal form that sells services to Google Ireland, or whether they act as an arm of the global business doesn’t necessarily change the margin – you can get to the same ‘right’ answer either way (through adjusting the transfer price to Ireland – which I think is what HMRC did).

If you think about how google ad-sales work – instantaneous auctions to see which adwords run, and pay per click for revenues – it makes sense to have contracts completed in as few places as possible – since ad-words bids put in from different places can be targeted wherever the advertiser choses, and compete against adwords bought in other places for placement. Its just not the kind of thing that lends itself to the kind of wholesale-retail structures we usually think of.

As well as the business rationale for why you would want to complete the sales in one place rather than force Google to establish a separate PE for each European country – it is also simpler for tax authorities in making the judgement on whether the margin is enough or not – essentially you have two numbers to compare – the fee the for service vs the cost to deliver it. It is not clear that trying to work out the margin on a host of individual ad-word sales is a better approach.

Perhaps I can suggest you read this http://uk.reuters.com/article/uk-tax-uk-google-specialreport-idUKBRE94005R20130501 . If “profits are earned by the hard working sales team in London” as you claim then you appear to have successfully defeated your own argument. A quick Duckduckgo and you might have come up with this http://www.bloomberg.com/news/articles/2010-10-21/google-2-4-rate-shows-how-60-billion-u-s-revenue-lost-to-tax-loopholes – a little out of date but makes the point that Google appear not to be paying significant corporate taxes anywhere and it is a fuller knowledge of the available facts that has created the suggestion that £130m is pitiful and derisory.

In relation to your first link, isn’t the point that in order to make the sales, the guys in London need to have something to sell? Much of that value is not created in the UK and so the point made above is that we don’t tax on turnover (as that would be an utter nightmare) but where value is created.

In relation to your second point, this is also addressed – for reasons of its own the US does not legislate to collect the taxes it could. Just because US value is not properly taxed does not mean that we should tax it here.

What Adam said!

I find Adam’s response to the second point deeply unconvincing.

Why would you treat some income as taxed if you don’t believe it has been? Abuse of such assumptions is exactly what leads to huge cash piles in the Bahamas waiting for the next repatriation holiday. I see no reason in principle not to require a receipt to obtain a tax refund.

The purportedly more credible estimate above should surely be including content acquisition in the UK cost base quadrupling the credible estimate and boosting Mr Maughm’s estimate only to 5%.

The HMRC should be starting negotiations on the basis of direct UK revenues less direct UK costs while expecting that reasonable allowances might bring the base down to global margins. Claims for further allowances ought to attract a great deal of scrutiny although enlightened policy might be generous where reciprocity is available and to our benefit.

The concept of value chain is not well defined in a way that is significant for the basic argument. US R&D does not create value from UK sales without UK sales and the there is no objective price for R&D rights between the marginal value of not providing it the whole revenue. Further the price and amount sold depends upon the organisation of concerned institutions.

This discussion might be helped by trying to identify several numbers.

– What did the law say?

– What did the law intend?

– What could the law intend? (Perhaps what is the highest rate that could be applied to Google that would not be directly against the interests of the UK?)

– What should the law intend? (How much would Google pay under rules that may extract less from Google than the answer to the previous question but from the uniform and reciprocal application of which the UK benefits?)

I think the answer to the first is less than £130m, the answer to the second considerably more and there is a clear case that Google has effectively paid a presumably beneficial amount to preserve a favourable tax regime. This is really not a great way of fixing things.

On a different note, do Google’s advertising revenues generate any VAT for the UK ? From what i can see, adwords invoices from Google Ireland to UK based companies have no VAT charged and Google’s UK customers add in a notional 20% VAT but then subtract that themselves on the same invoice by “charging” VAT (so-called “reverse-charging”). If the same customer buys advertising from a UK based billboard company (say) then that will (ultimately) generate VAT in the UK. Or am i missing something?

What about VAT on Google sales in the UK? Or is this a non-issue?

VAT should be a non-issue. Either UK or Irish VAT should be charged.

Business customers in the UK will operate the reverse charge on services received from outside the UK, and charge themselves 20% UK VAT. They can then recover that VAT on the same basis as VAT charged by a UK supplier.

Asssuming these are “electronically supplied sevices”, Google Ireland should be charging UK VAT on supplies to non-business persons since 2015. Before then, or if it was classified as “advertising services”, they should be charging Irish VAT, currently at 23%. A UK non-business person will not be recovering the VAT.

Excellent article Maya. My unusual combination of qualifications might enable me to offer some useful thoughts here – I’m an online marketing consultant for a Google Partner agency and a Chartered Accountant (although admittedly I was an auditor not a tax consultant).

As you’ve pointed out, the vast majority of Google’s revenues comes from advertising – and most of that is AdWords and AdWords-related stuff. Even most YouTube advertising is now done within AdWords. And by-and-large, AdWords revenue involves no Google salespeople, just automatic systems. There are some exceptions – such as the YouTube homepage masthead, which is sold by humans – and that’s what those London salespeople will be doing.

Because I run a Google Partner agency, I get to speak to Google AdWords experts (I spoke to my contact this afternoon in fact). They help me to help my clients by suggesting improvements to their AdWords campaigns. They aren’t really salespeople. And all the ones I speak to are in Dublin anyway.

When a web-user clicks on an AdWords ad, my client pays Google Ireland. I can sort of see an argument that if the click was made in the UK, then that should be considered as a UK sale, but that’s rather like saying that if the FA sells the TV rights to the FA Cup Final to Mongolian TV, then that revenue should be counted in Mongolia not in the UK.

In my opinion, UK companies are buying services from Google Ireland for the vast majority of UK AdWords clicks and that should be taxable in Ireland. One of the key purposes of the European Single Market is that a company in one country should be able to serve the whole Single Market. Those people arguing that all sales to UK customers should be deemed as happening in the UK would presumably advocate the UK leaving not just the European Union, but the Single Market as well. I don’t think any major UK political parties (not even UKIP) hold that view.

And of course, you make a very good point that the costs of those AdWords sales are things like the R&D that was almost all done in California, and that therefore any sales of AdWords made by Google’s international subsidiaries should be accompanied by costs of those sales in the local accounts. To not do so would seem to be distorted reporting.

Is there a VAT issue here too?