If no one thinks that country-by-country reporting can raise a trillion Euros, why pretend it can?

11Nov15

I did not start this blog with the intention of endlessly cataloguing strange-numbers-and-weird-beliefs in the international tax avoidance debates, but since I have taken on the role of the child-who-missed-the-memo-about-the-Emperor’s-New Clothes, I guess I have to keep pointing them out when they stride past.

Last week the king who was in the altogether was Transparency International, the grandfather of transparency and anti-corruption advocates, a usually sober organisation which takes its own accountability seriously

Transparency International’s Brussels team put out a video on the issue of multinational tax avoidance which makes the case for public country-by-country reporting; highlighting the issue of profit shifting, the ‘lux leaks’ scandal and state aid cases involving Fiat and Starbucks. (its about 3 minutes)

‘The potential impact of such deals is huge’

After introducing the topic the video says

“The potential impact of such deals is huge; In the EU alone 1 trillion Euro is lost each year by tax evasion and avoidance, luckily there is a solution…. ”

Hold up. A trillion Euros a year is not just huge, its huuuuuuuge. It is more than double the total amount of corporation tax that European governments collect from domestic and multinational companies combined. It is around 20 times what is implied by the OECD’s recent estimate of global Base Erosion and Profit Shifting, or 7 times the equivilient figure that Ernesto Crivelli, Ruud De Mooij and Michael Keen at the IMF come up with (*warning: back of an envelope calculations– see below).

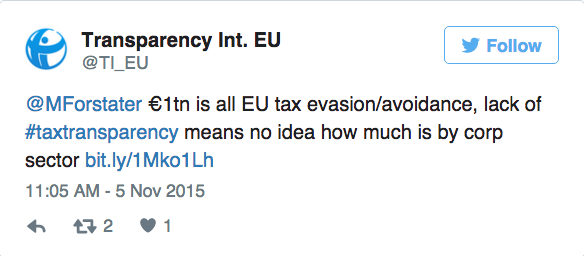

What is 1 trillion doing here? TI responded on Twitter (we have also emailed) :

But we do have an idea. We know about the scale of existing corporate tax revenues, and we know from the small cannon of studies on base erosion and profit shifting that there are other numbers, smaller by an order of magnitude, which could reasonably have been used.

We also know the basis for the estimate they did use. It is indeed an estimate of ‘evasion and avoidance’. In fact the report by Richard Murphy makes clear that it is mainly about tax evasion in the shadow economy (i.e. undeclared and hidden income – largely the cash economy). 85% of the 1 trillion figure is based on a calculation which multiplies estimates of the size of the shadow economy in each country in Europe by the overall tax burden as a percentage of GDP.

It is a good-faith, back-of-envelope effort to estimate overall tax evasion, which can be questioned on its own terms – how reliable are the shadow economy estimates on which it depends?, is it reasonable to assume that activities in the shadow economy are evading all taxes rather than just some (e.g. paying VAT, fuel duty, local rates etc… but avoiding income tax on profits or wages)? What about the behavioural impacts of taxing the grey economy?

These are interesting questions. The question of whether €1 trillion is a good estimate of base erosion and profit shifting by multinational companies in Europe is not. No one has ever seriously said it is. Not Richard Murphy. Not anyone.

Bidding up the case for country-by-country reporting

Transparency is generally a good thing. But we are at the early stages of understanding how to make sense of country-by-country reports. Personally, I am not convinced that CBCR will deliver the large fiscal boost that many have hoped for. Arguments that public CBCR can do everything from enhancing tax compliance, to creating moral suasion for corporations to pay the ‘right’ amount of tax beyond compliance, to exposing corruption to creating pressure for changes to the tax system seem a bit oversold.

This is not necessarily an argument against CBCR, but for PDIA (problem driven iterative adaptation – getting serious about trying and learning before declaring to have found a universal solution). It makes me nervous that a culture has built up in the debates around this instrument, where it is normal to exaggerate its potential, and where there are strong social pressures not to question such exagerations.

Transparency International’s values include commitment to disseminating information that is reliable, verifiable and up-to-date and to take positions based on sound, objective and professional analysis and high standards of research. But on this topic they go ahead with a patently silly number. As I have written before, there is a problem here, which goes beyond TI.

The dilemma for transparency as a theory-of-change is that we can always push for more data, it is the easy moral high ground. What is harder is to develop meaningful analysis of what the disclosures show. One good example of this was the case of the leaked oil and gas contract in Tanzania last year where the Natural Resource Governance Institute stepped up to provide some technical analysis to inform debate, after initial media and political estimates suggested that Tanzania was being stiffed for $1 billion.

If multiple organisations crowd into the echo chamber bidding up expectations to impossible levels, who will act as accountable and robust sources of expertise to do the analysis and help the public make sense of the issues?

(* back of an envelope calculation.s If EU GDP is 14 trillion Euros and corporate tax is around 3% of GDP then corporate tax in Europe is 420 billion Euros. The OECD estimate that BEPs amounts to 4 to 10% of corporate tax- so 17- 42 billion Euros. Crivelli, De Mooij and Keen put it at around 1% of GDP in OECD countries – or around 140 billion Euros)

Filed under: Uncategorized | 4 Comments

I think your blogs SHOULD be reported as widely as these widely overstated estimates. Unfortunately big numbers, no matter how baseless are sexy and attention grabbing.

Keep up the good work, because at some point the “tax dodging” tide will recede and the public will see you are the only one wearing a swimsuit.

I’m not convinced that we won’t just see a move from revenue shifting (Google recording UK sales in Ireland) to cost shifting (Starbucks transfers for IP rights), either way the profit ends up where the multinational wants it to be.

Costs and transfer pricing is easier to challenge and there are established rules, but I’m dubious it will be that much of a tax generating target for authorities to the extent that some claim for CBCR