Looking for MTNs ‘Offshore Stash’

16Oct15

Last Friday a story appeared in the national press in South Africa, Ghana and Uganda with headlines about ‘MTN’s offshore billions’. It appeared to reveal a secret ‘stash’ of money built up by the company behind a brass-plate shell company in Mauritius.

“The Finance Uncovered global network of investigative reporters have today published a cross-border investigation into South African telecoms giant MTN exposing how billions of rand from its subsidiaries in Ghana, Nigeria and Uganda have been shifted to a shell company in the small island tax haven of Mauritius.”

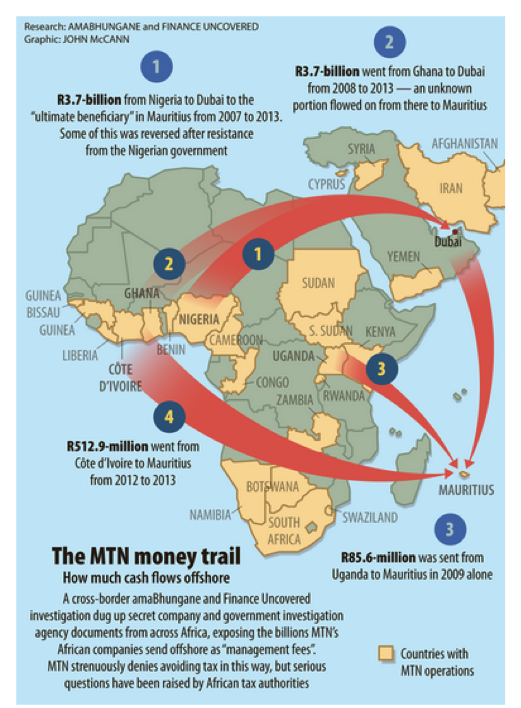

Follow the red arrows…

I have written about some of the confusion and misperceptions around the big number estimates of international tax dodging, but I am wary of jumping in to ‘defend’ individual companies. There are lots of reasons not to. They can defend themselves. People will roll their eyes and say “there she goes again, helping the tax dodgers”. And if it turns out to be the next Petrobras scandal-in-waiting, I will look pretty silly, gullible or even mendacious.

But still, it’s a serious charge and deserves looking at seriously. If MTN are finagling to artificially shift profits to low-tax destinations there are questions to be answered. It they are illicitly concealing them in a secret offshore ‘stash’ that is really serious. But what if their accounts simply reflect what it looks like when you undertake the complex, legitimate and hugely important business of bringing capital, technology, cash-flows and know-how together to build mobile phone services across 21 countries in Africa and the Middle East?

Finance Uncovered

The investigation into ‘MTN’s Mauritian Billions was carried out by a group of journalists with support and training from the ‘Finance Uncovered’ project established by the UK based Tax Justice Network, with funding from the Joseph Rowntree Charitable Trust and Oxfam Novib. It provides training and support from tax campaigners to journalists who want to investigate illicit finance. They seem pretty convinced that something dodgy is going on.

But reading their report, and MTN’s responses to their questions I find it hard to see what. There does not appear to be anything there that is both scandalous (i.e. hidden or inappropriate) and a tax benefit to MTN.

Clearly there is a tax advantage to chosing to siting some shared service operations in Dubai, but its hardly a scandalous practice simply to have operations in Dubai.

The main revelation, which Finance Uncovered see as a smoking gun is that:

“most of the money, which MTN badged as “management fees”, ended up on the Indian Ocean island of Mauritius, where the company employs no staff and appears to own little more than a postbox.”

“The Mauritian entity employs no staff and cannot, therefore, physically provide a service” says the South African Mail & Guardian’s Centre for Investigative Journalism. As Finance Uncovered notes companies have been known to lower their corporate tax bills by shifting revenues from a high-tax country to a tax haven such as Mauritius.

So this is what we think happened, right?

Where’s the beef?

It sounds damning. However the report acknowledges further down the page that MTN say that they are not avoiding tax in this way. MTN say the payments received in Mauritius are used to pay for group services in South Africa and to service external debts, with any cash remaining returning as dividends to South Africa. Furthermore, the Mauritius entity is tax resident in South Africa and is subject to South African not Mauritian taxes and tax treaties.

There just doesn’t seem to be any actual evidence for hidden ‘stashes’ of cash in Mauritius.

Certainly there may be questions from Uganda, Ghana and other countries where MTN has subsidiaries about whether the price is right on contracts for technical services, and the report highlights processes where they are awaiting approval on fees, or the levels have been challenged by the authorities each country.

But overall it doesn’t look like MTN is achieving an inordinately low tax rate. Its accounts say that its effective tax rate has ranged from 26 to 38% over recent years, amounting to 13 billion rand in 2014 (South Africa’s statutory rate of corporate income tax is 28%). Its not a perfect indicator, but it hardly seems to support a conclusion of rampant corporate tax avoidance.

Despite the lack of strong evidence, the reporters, and the organization advising them seem to be telling us to assume that intra-company transfers must be dodgy. This is worrying, as any company undertaking FDI into Africa, and drawing on international technology, capital and management capacity will engage in transfer pricing. This in itself cannot be enough to make a company fair game for being portrayed as a corrupt and tax avoiding.

My fear is that creating a perception of tax dodging and corruption on such scant evidence and strong assumptions does nothing to address really corrupt dealings, but could make investment environments less attractive for companies that that value their reputation for integrity. Reinforcing the perception that ‘everyone is at it’ undermines trust in both business and public institutions and could discourage the voluntary compliance on which tax systems depend. Our trust in NGO and media investigations themself is also a critical and non-renewable resource in uncovering corruption – it should not be squandered by ‘crying wolf’.

The idea of an international network to support and train journalists to investigate illicit finance is a good one. (There is also a similar project, Wealth of Nations, run by the Thomson Reuters Foundation, with funding from NORAD). Efforts to increase the quantity and quality of public scrutiny, debate and understanding on tax issues, financial flows and corruption are valuable. They could bring in a broader set of tax experts to help them test their analysis and conclusions.

Perhaps there is something to find here, and they just haven’t found it yet. But readers deserve more than big red arrows of innuendo pointing them to jump to palm fringed-conclusions.

Filed under: Uncategorized | 5 Comments

Maya,

Thanks for taking the time to read and comment on our investigation.

Your criticism that the group level tax rate is evidence that MTN is not engaging in tax avoidance we feel is misplaced, because the group level tax rate is manifestly not the issue we were dealing with in our investigation.

In the context of profit shifting, the group level rate is irrelevant because profit shifting erodes the tax base. It has no impact on the tax rate. In other words, if a company is engaged in profit shifting it lowers the amount of profit that the tax rate is applied to.

To be doubly clear, you could be paying a 90% tax on £1. The fact that there is a 90% rate on that £1 does not mean you haven’t been engaging in tax avoidance if the taxable amount should have been more than £1.

We feel that the story was very clear. The investigation questioned whether MTN was extracting profits fairly from companies they owned outside of South Africa. In this case, the main issue is not the total group level tax rate for MTN as a whole, but the tax base in the countries where it operates.

It matters very little to people in Uganda, Nigeria, Ghana and Cote d’Ivoire if profits extracted from their countries are then taxed in South Africa. Their interest is that the company is properly taxed in their home countries.

You say that there is scant evidence of tax avoidance. Our article found billions of rand being paid to a shell company in Mauritius for management services, and government authorities from several countries challenging these payments. One country is taking court action. The fact that these payments were made to a company with no employees raises legitimate questions regarding their substance.

Although MTN told us that some of those payments were remitted from Mauritius to South Africa, they refused to tell us how much. We gave them every opportunity to do so. MTN did admit that not all of the fees were remitted to South Africa.

We are sure that people can make their own minds up about the payments. And we feel strongly that reporting on this ongoing and live issue is eminently newsworthy.

Of course you know all this, because we set this out to you in the long email correspondence we had over the last week.

In response, you told us that we had misunderstood the issue, because in your words, “Use of the words ‘management fees’ does not imply that the money must be passed through and used to ‘pay managers’ – it is used to describe a professional service contract between two companies”. It would be interesting to know what professional services you think MTN International (Mauritius) renders if it has no staff.

We note that this is not an argument you advance in your blog.

It is illustrative that your blog frequently tells the reader what we “seem to be” saying, but nowhere have you mentioned that you contacted us to clarify what we said, and that we responded to you in full.

We have been more than willing to engage with you, to help you understand our story and to spend time making sure we were as clear as possible with the questions you asked us.

That you continue to choose to repeat your misunderstandings of the article, without including our view, is disappointing, particularly in the context where you accuse others of using innuendo to mislead the reader.

For our part, we have been meticulous about the information we have gathered, and amaBhunghane published in full the correspondence they had with MTN.

Finally, a question for you: within hours of publishing our article last week, you took to social media to attack it. You first accused us of being a ‘sock puppet’ and asked questions about our funding which we answered. When that failed as a line of attack you said that the tax rate paid by MTN shows that our investigation was unfounded – an issue we have dealt with. Rather than acknowledge that, you continued to publish your blog post without acknowledging our position.

What is your interest in this? Maybe it is an attempt to bring clarity to this important debate. If that is the case, we hope we have now helped you and your readers in that mission.

Dear George Turner

Thank-you for responding.

And yes, thank-you to Nick Mathiason for corresponding by email when I sent him a draft of the blog-post last week. We exchanged notes and questions, I thanked him and he signed off with “I look forward to reading the blog” so yes I did continue to publish the revised blog post. I also sent the draft to a couple of other people who commented, but I don’t tend to quote private emails or include acknowledgements sections in blogposts.

Yes I did also ask about Finance Uncovered’s funding and connection to Tax Justice Network on Twitter because the Finance Uncovered website gives no clue. (Seriously, tax justice dudes: asking an organisation for some really basic information about itself is not ‘a line of attack’) . Alex Cobham of TJN assured me that although Finance Uncovered started as a TJN project, it is now freestanding. He asked me why I wanted to know and I responded “Website is a bit mysterious. No info. Feels a bit sock-puppety”. Later Nick Mathiason of Finance Uncovered said that it is actually a TJN project but plans to become independent next year. A basic explanation on the Finance Uncovered website would offer transparency to readers (and would clear up internal confusion).

Now I hope I have justified myself enough to talk about substance….

I do not think the presentation of the story is clear. It is presented as a story about an offshore stash of ‘Mauritian Billions’. For example your Mail and Guardian article leads with, and emphasises as a pull-out quote, the statement that ‘By shifting revenues from a high-tax country to a tax haven, a company can lower its corporate tax bill’ – suggesting that the issue that you think you found here is BEPS-type avoidance. But as you yourself say over at TJN (http://www.taxjustice.net/2015/10/14/the-offshore-wrapper-a-week-in-tax-justice-70/) your own nuanced interpretation is quite far from the ‘offshore stash’ headlines. i.e. “if what MTN say is true, and all the revenues moved to Mauritius are taxed in South Africa, then this is perhaps less a story about the taxes MTN pays, but rather a distributional issue between South Africa and other African countries.” (I would agree)

I did not say in the blog post that the group level tax rate is ‘evidence that MTN is not engaging in tax avoidance’ I said that ‘Its not a perfect indicator, but it hardly seems to support a conclusion of rampant corporate tax avoidance’. It is not hard evidence either way but I think it is a salient piece of information in putting MTN’s tax affairs into context. It tends to push the conclusion more towards the ‘distributional issues’ reading rather than the ‘stashing billions in tax havens’ headlines. Had it been included in the articles readers could make that judgment themselves rather than assuming it must be low, to match the avoidance headlines, or having to go and look it up themselves.

You say ‘It matters very little to people in Uganda, Nigeria, Ghana and Cote d’Ivoire if profits extracted from their countries are then taxed in South Africa.’ Here I simply disagree. We don’t know whether profits are being extracted to South Africa, or whether the fees are compliant with transfer pricing rules (that is for the Ugandan courts, for example, to determine), but people in Uganda, Nigeria, Ghana and Cote d’Ivoire have as much interest as people anywhere else in knowing whether companies investing there are carrying out BEPs-type behaviours or are more simply involved in complex value chains where there are tensions and uncertainties about where value should be deemed to be created and taxable.

Of course every country would prefer to include more of the taxbase of the value chains they are involved in there own jurisdiction, but the problem of double taxation is real – if companies face the prospect of unpredictable and/or double taxation it makes investment less attractive and raises the cost of capital. Having mobile phone networks is unashamably a good thing for development. This really does matter to countries like Uganda, Nigeria, Ghana and Ivory Coast, even if it is only tax nerds who worry about the distinction between transfer pricing and transfer mispricing, or between an entity that is tax resident offshore and one that is not.

I recognise that having already published these reports it would be unwise of you to engage in any discussion that does not 100% stand-by the original presentation so we are unlikely to have a fruitful discussion at this point, despite us both, I am sure, being nice people with the best of intentions, who in another situation could discuss the nuance of the issues without snipping.

This is a problem, because such cases often become cited and re-cited, until they become an accepted ‘fact’ which shapes understanding, despite there having been no independent scrutiny or analysis beyond the original scandal-and-denial reporting (this in answer to your question is my interest – and why I have stuck my neck out to write about it). I support Finance Uncovered’s mission to increase the quality and quantity of coverage on these issues – I hope that as the organisation becomes independent it expands the sphere of experts that it draws on to speak at trainings and to provide a network of support to journalists – I think there are quite a few out there who would do this – it could provide a valuable forum to test and debate conclusions in a less adversarial manner before publication, which could only enhance the quality and confidence of analysis.

“In the context of profit shifting, the group level rate is irrelevant because profit shifting erodes the tax base. It has no impact on the tax rate. In other words, if a company is engaged in profit shifting it lowers the amount of profit that the tax rate is applied to.

To be doubly clear, you could be paying a 90% tax on £1. The fact that there is a 90% rate on that £1 does not mean you haven’t been engaging in tax avoidance if the taxable amount should have been more than £1.”

that’s rather badly put. Of course the point of profit shifting is to reduce the group ETR, so hardly irrelevant in this context.

I think what you mean is that you cannot deduce much about profit shifting out of (small) territories from the (large) group ETR.

The example involving 90% on £1 base does not clarify things, when talking about group ETR because BEPS is not about reducing group taxable profits. What you write about 90% would make sense if we were looking at ETRs in territories where profits are shifted out of – there it would indeed be irrelevant.

“In the context of profit shifting, the group level rate is irrelevant because profit shifting erodes the tax base.”

To echo Paddy Carter, this is very badly put – if not plain wrong.

Profit shifting erodes the tax base in any particular jurisdiction.

However, ETR is calculated based on the overall group’s accounting profits. For ETR purposes, the accounting profits *are* the “tax base”, and unaffected by BEPS.

That is, if you shift profits from Uganda to Mauritius you erode Uganda’s tax base, but the group’s tax base (to the extent that this is a valid concept) remains the same.

Thanks Paddy and Andrew

Yes that was my point – there seems to be a fundamental confusion on the part of finance uncovered here:

“In the context of profit shifting, the group level rate is irrelevant because profit shifting erodes the tax base. It has no impact on the tax rate. In other words, if a company is engaged in profit shifting it lowers the amount of profit that the tax rate is applied to.”

– this is true at the level of the subsidary, but not at the group level, where a company has no interest in eroding its own overall profits.

I think you are right Paddy, in terms of not being able to work out what is going in small jurisdictions by looking at the group tax rate. But given that, for example Nigeria is the company’s largest market (2014 AR says responsible for 48% of EBITDA) you would expect that if the company was reducing achieving BEPS-type double non-taxation or low tax levels by shifting profits this would show up in a low overall ETR.

———

On the other hand if there was an illicit ‘stash’ of funds hidden from the South African tax authorities (and from shareholders) then this WOULD result in tax losses without reducing the overall ETR – but this would be corruption/fraud.

I don’t think this is was Finance Uncovered is alleging – but the suggestion that the overall ETR is irrelevant only seems to be consistent with the idea that there is a ‘stash’ of hidden profits which can not be seen from looking at the public accounts.